With gold prices holding steady for months above US$1,300 per oz., and years of painful cost-cutting and writedowns now firmly in the past, the mood of gold miners in attendance at this year’s Denver Gold Forum put on by the Denver Gold Group at the Broadmoor in Colorado Springs in late September was the best since September 2012, when gold prices first marched south from their heady levels of US$1,800 per oz. to multi-year lows of US$1,050.60 per oz. in December 2015.

Despite the rosier outlook, gold miners still appear scarred from the last four years of weak gold prices and capital markets. Two recurring themes in the presentations of the world’s largest gold miners were the need for vigilance with respect to cost control and discipline in the arena of mergers and acquisitions, after the wild buying binge from 2006 to 2011, followed by the four-year purge from 2012 to 2015.

Kelvin Dushnisky, president of Barrick Gold, said that after years of divestments, his firm can focus on its five core mines (Goldstrike and Cortez in Nevada, Pueblo Viejo in the Dominican Republic, Lagunas Norte in Peru and Veladero in Argentina), which will produce 70% of its production in 2016, and work to keep its position as the lowest-cost producer amongst its major competitors, at an all-in sustaining cost (AISC) of US$750 to US$790 per oz. this year.

Despite the company’s shrinkage over the past two years, Barrick still has the largest gold reserve base of 91.9 million oz. gold in 2.2 billion tonnes at 1.32 grams gold per tonne. Moreover, he noted Barrick has kept a company-wide, 16-year mine life ahead of it for the past 20 years, and is using a long-term gold price of US$1,200 per oz. when it allocates capital.

Newmont Mining’s president and CEO Gary Goldberg similarly touted his firm’s three-and-a-half-year effort to improve its assets and business model, which has resulted in longer-life and lower-cost gold mines, with Newmont’s AISC dropping 28% from 2012 to a projected US$852 per oz., even with its dependence on U.S. mines that couldn’t benefit from currency devaluations seen in so many other gold-mining jurisdictions.

Newmont’s high-profile divestments in recent years have included Batu Hijau in Indonesia, Midas in Nevada, Jundee in Australia, Penmont in Mexico and Waihi in New Zealand.

One of its biggest accomplishments this year is bringing into production its 75%-owned Merian gold mine in Suriname on schedule and US$100 million under budget at a capital cost of US$575 to US$625 million. Commercial production is set to start in the fourth quarter, ramping up to an annual rate of 300,000 to 375,000 oz. gold at AISC of US$650 to US$750 per oz. gold.

AngloGold Ashanti’s chief operating officer Ron Largent similarly talked about the firmer financial foundation of the company after three years of cuts and asset sales. But he also detailed AngloGold’s emphasis on “optionality” and free cash flow rather than growth, even as he argued that “we haven’t changed our strategy.”

With 19 operations in nine countries, AngloGold today derives 95% of its revenue from gold, and has what Largent calls a strong pipeline of brownfield and greenfield projects. AngloGold has cut its AISC by 40% over the past two years to US$910 per oz. this year, which puts it in a position to resume its dividend in 2017 after a three-year hiatus.

Russell Ball, Goldcorp’s executive vice-president, chief financial officer and corporate development, who replaced new president and CEO David Garofalo at the last minute as speaker due to a “family medical issue” and “very difficult situation,” said Goldcorp is focused on its “clear vision” of annual gold production of 3 to 4 million oz. gold from six to eight large-scale mining camps in Western Hemisphere jurisdictions with low political risk.

He hinted there may be some trimming of the company’s asset base “in the long-term” to meet the company’s criteria of each camp producing 400,000 to 500,000 oz. gold to Goldcorp’s account.

With respect to the recent acquisition of Kaminak Gold and its Coffee gold project in the Yukon, Ball said “we didn’t buy it for the 200,000 oz.” per year of production in Kaminak’s feasibility study, and that “we think we can grow Coffee into a camp for us.”

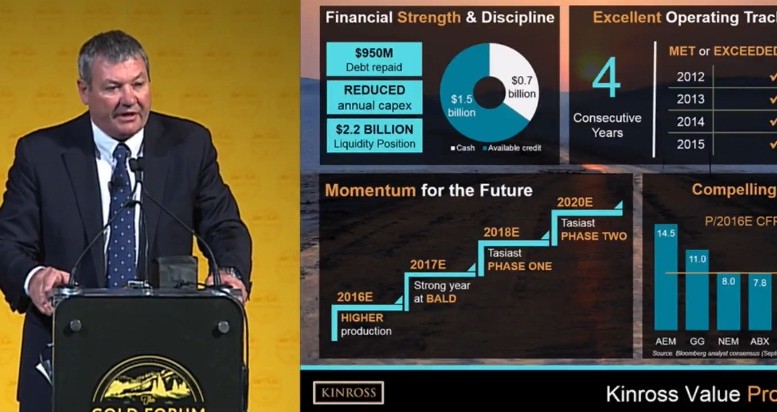

Kinross Gold CEO Paul Rollinson put focus on what he argued is his company’s “culture of technical excellence and fiscal conservatism.”

Over the last four years, he noted, Kinross has consistently met its annual and quarterly production guidance, which stands at 2.7 to 2.9 million equivalent oz. gold in 2016, up from 2.6 million equivalent oz. gold in 2015, with AISC at US$890 to US$990 per oz. from US$975 per oz. in 2015. Kinross is proceeding with a first phase of growth at its difficult Tasiast gold mine in Mauritania, and expects to reach full production there in the second quarter of 2018.

Be the first to comment on "Editorial: Gold miners find room to breathe"