A prolonged Iran conflict could push copper into surplus and sharply cut earnings for major producers, according to Bloomberg Intelligence.

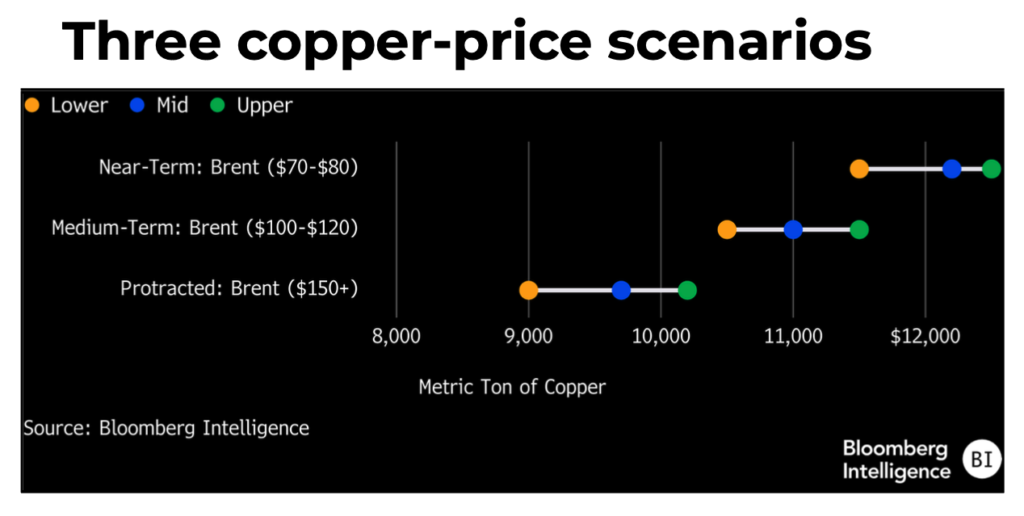

Oil above $150 a barrel in a drawn-out war that disrupts Strait of Hormuz flows would likely slow global growth and cap copper demand at about 0.5%–1%, driving prices below $10,000 a tonne and leaving a refined surplus of 100,000–200,000 tonnes, BI analysts said.

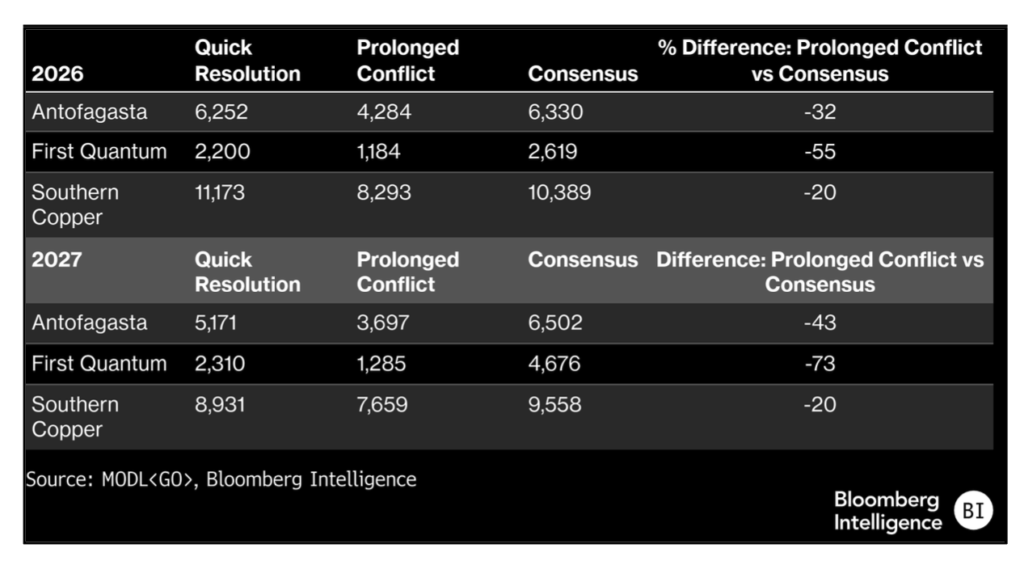

Under that scenario, earnings could fall about 20% at Southern Copper (NYSE: SCCO), 32% at Antofagasta (LSE: ANTO) and as much as 55% at First Quantum (TSX: FM), reflecting higher costs and weaker pricing than consensus forecasts assume. Global benchmark Brent crude was up 3.3% on Tuesday morning to more than $103 a barrel.

Southern Copper appears best positioned in a downside scenario due to its low-cost base, while First Quantum faces the greatest risk given its higher cost profile and uncertainty around the restart of Cobre Panama, which consensus expects to contribute meaningfully by 2027.

If the war extends beyond a year and Hormuz flows remain constrained, cooling demand would expose the cost curve and leave higher-cost producers most vulnerable.

“While copper’s long-term fundamentals remain intact, near-term pricing and margins are highly sensitive to energy-driven inflation and supply disruptions,” Grant Sporre, global head of metals and mining at BI, said.

The outlook underscores how geopolitical risk in the Middle East could ripple through commodity markets, with copper caught between slowing demand and constrained supply inputs such as sulphur. Even as the global economy becomes less dependent on oil, higher energy prices would likely revive inflation, delay rate cuts and weigh on industrial activity, limiting copper’s upside while tightening margins across the mining sector, the analysts warn.

Multi-month scenario

A multi-month conflict would be less damaging, with copper markets roughly balanced in 2026 and prices in the $10,500–$11,500 range, while a quick resolution could restore a modest deficit and support prices near $12,000. Rising inventories, now near 1.4 million tonnes, signal weaker demand and a buyer’s market, suggesting any rally may be capped until stockpiles normalize.

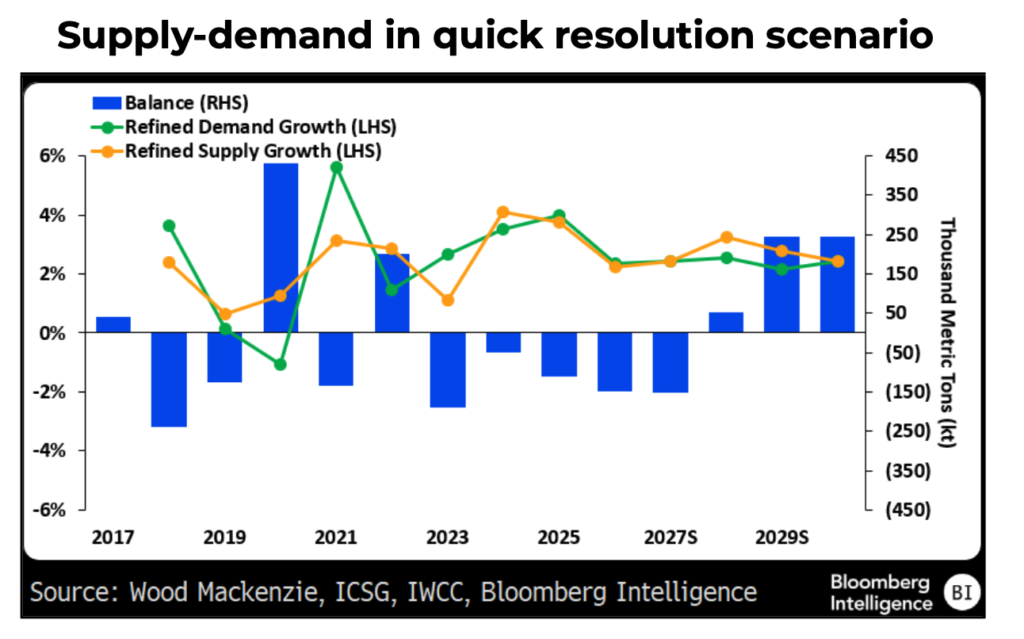

BI analysts had already expected slower global demand growth of 2%–2.3% in 2026 as high prices curb affordability, and warn it may be difficult to lift mined supply even with a 1.1 million-tonne disruption allowance as stoppages persist at major operations.

Supply risks could partially offset the downside. Disruptions to sulphur shipments from the Persian Gulf may constrain output in the Democratic Republic of Congo, where 50%–60% of production depends on sulphuric acid, limiting the scale of any surplus.

Persistent mine disruptions and tight concentrate markets could also make it difficult to lift supply meaningfully in 2026.

Higher costs remain a central concern. BI estimates a prolonged conflict could lift unit costs by 10%–20%, with sulphuric acid and other inputs driving broader inflation. High-cost producers may see margins compress to about 40% in 2026 from roughly 70% in 2025, with all-in margins nearing long-run averages, raising the risk of reduced capital spending and delayed project approvals.

The China factor

China’s demand outlook adds further uncertainty. BI’s proxy for Chinese copper demand fell to a multi-year low late last year, pointing to growth of just 0.5–1% in 2026, well below 2025 levels, as property weakness and softer industrial activity weigh on consumption.

The broader takeaway is that copper’s structural deficit story may be delayed rather than derailed, as short-term geopolitical shocks reshape demand, costs and investment timelines across the industry.

Be the first to comment on "Prolonged Iran war would hammer top copper miners"